All Categories

Featured

Table of Contents

Another kind of advantage credit scores your account balance occasionally (annually, for example) by setting a "high-water mark." A high-water mark is the greatest value that a financial investment fund or account has actually gotten to. Then the insurer pays a fatality benefit that's the higher of the bank account value or the last high-water mark.

Some annuities take your initial financial investment and immediately add a specific portion to that amount yearly (3 percent, as an example) as an amount that would certainly be paid as a survivor benefit. Annuity investment. Recipients then get either the actual account value or the first investment with the annual boost, whichever is greater

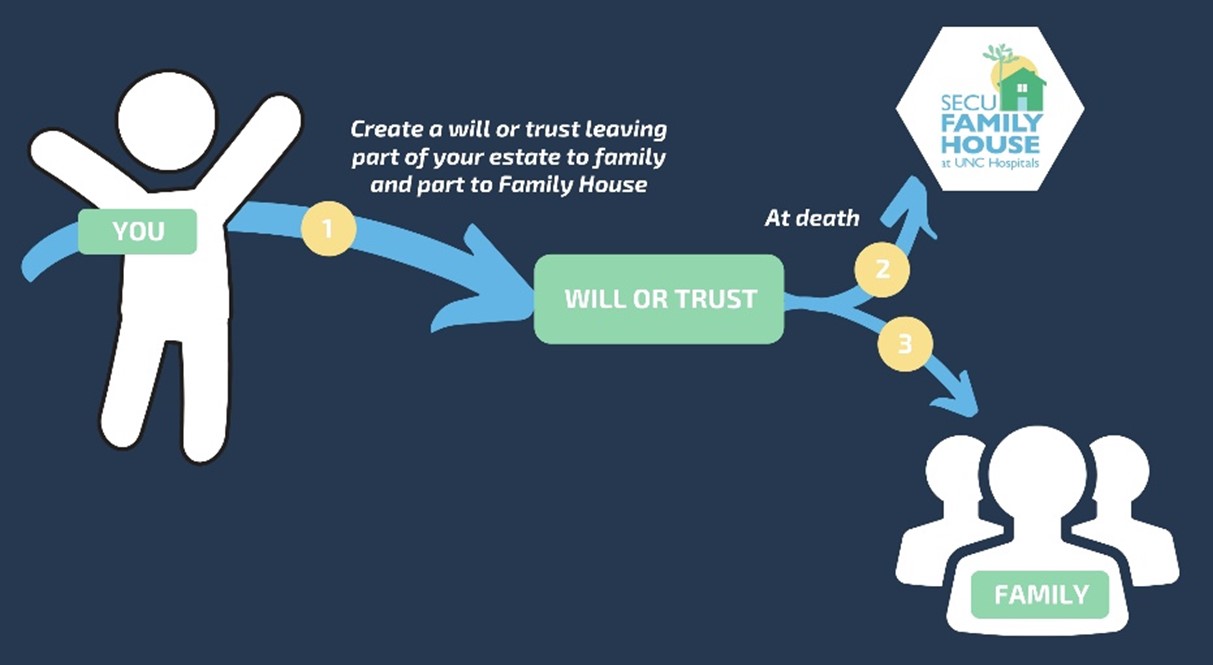

You can select an annuity that pays out for 10 years, yet if you pass away before the 10 years is up, the staying payments are ensured to the recipient. An annuity fatality advantage can be practical in some situations. Below are a few instances: By aiding to stay clear of the probate process, your beneficiaries might obtain funds promptly and easily, and the transfer is private.

How long does an Annuities For Retirement Planning payout last?

You can typically pick from several choices, and it's worth discovering every one of the choices. Pick an annuity that works in the manner in which ideal helps you and your family members.

An annuity aids you build up money for future revenue requirements. The most suitable use for earnings settlements from an annuity agreement is to fund your retirement.

This product is for informative or academic objectives just and is not fiduciary financial investment recommendations, or a safeties, financial investment strategy, or insurance coverage item recommendation. This product does rule out a person's own goals or circumstances which must be the basis of any type of financial investment decision (Guaranteed income annuities). Investment items may be subject to market and various other risk aspects

What are the tax implications of an Fixed Vs Variable Annuities?

All assurances are based upon TIAA's claims-paying ability. Fixed annuities. TIAA Traditional is an assured insurance contract and not a financial investment for federal safeties law objectives. Retirement repayments refers to the annuity earnings obtained in retirement. Guarantees of taken care of regular monthly settlements are just connected with TIAA's repaired annuities. TIAA may share profits with TIAA Standard Annuity proprietors via declared additional amounts of passion during accumulation, higher preliminary annuity income, and through additional rises in annuity earnings benefits throughout retirement.

TIAA might provide a Loyalty Incentive that is just readily available when electing life time earnings. Annuity contracts may contain terms for maintaining them in force. TIAA Traditional is a fixed annuity product provided with these agreements by Educators Insurance and Annuity Organization of America (TIAA), 730 Third Avenue, New York, NY, 10017: Type collection including but not limited to: 1000.24; G-1000.4; IGRS-01-84-ACC; IGRSP-01-84-ACC; 6008.8.

Transforming some or every one of your financial savings to income advantages (referred to as "annuitization") is a permanent decision. When income advantage settlements have actually started, you are incapable to alter to another alternative. A variable annuity is an insurance contract and includes underlying financial investments whose worth is linked to market efficiency.

Is there a budget-friendly Fixed-term Annuities option?

When you retire, you can select to obtain revenue permanently and/or various other revenue choices. The genuine estate sector goes through different threats consisting of fluctuations in underlying residential or commercial property values, costs and earnings, and possible environmental obligations. As a whole, the worth of the TIAA Property Account will fluctuate based on the underlying worth of the straight genuine estate, genuine estate-related investments, actual estate-related protections and liquid, set income investments in which it invests.

For an extra full discussion of these and various other dangers, please seek advice from the syllabus. Responsible investing integrates Environmental Social Administration (ESG) elements that may influence direct exposure to companies, fields, sectors, restricting the kind and number of financial investment opportunities offered, which could result in excluding investments that perform well. There is no warranty that a diversified portfolio will boost general returns or exceed a non-diversified portfolio.

Accumulation Bond Index was -0.20 and -0.36, specifically. Over this very same duration, connection between the FTSE Nareit All Equity REIT Index and the S&P 500 Index was 0.77. You can not invest straight in any kind of index. Index returns do not show a reduction for costs and expenditures. Various other payment alternatives are offered.

There are no costs or costs to start or quit this attribute. It's important to note that your annuity's balance will be reduced by the revenue settlements you receive, independent of the annuity's efficiency. Revenue Examination Drive revenue settlements are based upon the annuitization of the amount in the account, duration (minimum of ten years), and various other elements chosen by the participant.

What should I look for in an Tax-deferred Annuities plan?

Annuitization is unalterable. Any type of warranties under annuities provided by TIAA are subject to TIAA's claims-paying capacity. Interest in unwanted of the assured amount is not ensured for periods aside from the periods for which it is proclaimed. Converting some or every one of your cost savings to income benefits (described as "annuitization") is a permanent choice.

You will have the alternative to call multiple recipients and a contingent beneficiary (somebody designated to obtain the cash if the primary beneficiary passes away prior to you). If you don't name a beneficiary, the accumulated properties can be surrendered to a banks upon your death. It is very important to be knowledgeable about any financial repercussions your recipient may encounter by inheriting your annuity.

Your spouse could have the option to alter the annuity agreement to their name and come to be the new annuitant (known as a spousal continuation). Non-spouse recipients can not proceed the annuity; they can only access the marked funds.

What does an Annuity Riders include?

In many cases, upon death of the annuitant, annuity funds pass to an effectively named recipient without the delays and expenses of probate. Annuities can pay fatality benefits numerous various methods, depending on regards to the contract and when the death of the annuitant occurs. The alternative chosen effects exactly how tax obligations schedule.

Picking an annuity beneficiary can be as complex as selecting an annuity in the initial place. When you chat to a Bankers Life insurance coverage agent, Financial Agent, or Investment Advisor Agent who offers a fiduciary requirement of care, you can relax ensured that your decisions will aid you construct a strategy that provides protection and peace of mind.

{kind=link}

Table of Contents

Latest Posts

Analyzing Strategic Retirement Planning Everything You Need to Know About Financial Strategies Breaking Down the Basics of Investment Plans Pros and Cons of Deferred Annuity Vs Variable Annuity Why Fi

Highlighting the Key Features of Long-Term Investments A Comprehensive Guide to Investment Choices Defining the Right Financial Strategy Features of Fixed Vs Variable Annuity Pros Cons Why Fixed Vs Va

Analyzing Strategic Retirement Planning Everything You Need to Know About Financial Strategies What Is Variable Vs Fixed Annuities? Benefits of Fixed Vs Variable Annuity Pros And Cons Why Pros And Con

More

Latest Posts